- The Blueprint

- Posts

- The spring housing season is off to a sour start

The spring housing season is off to a sour start

Plus, the share of sellers cutting their asking prices hits a new record

Rinku Mathew

April 15, 2026

A mismatched market

As you’ll see below, the share of listings with price cuts has climbed to its highest level since 2012 — a clear signal that sellers are adjusting to market reality.

Buyers have more leverage than they’ve had in years. But that leverage isn’t translating into deals.

Concerns about the economy, job security, and broader geopolitical uncertainty have led nearly 30% of Americans to delay major purchases, including homes.

The result: a mismatched market where buyers have the advantage but are hesitant to make a move.

In today’s newsletter, we’ll break down how agents should approach this market and what opportunities are out there despite all the uncertainty

- David

The spring housing season is falling short of expectations

Source: Unsplash

Existing home sales fell 3.6% in March to a seasonally adjusted annual rate of 3.98 million, the lowest level since June 2025 and well below expectations. According to the Wall Street Journal, the 3.6% month over month decline was much worse than the 1% drop forecast by housing economists. It was the second-largest monthly decline in the past year.

Here’s what else the Journal reports:

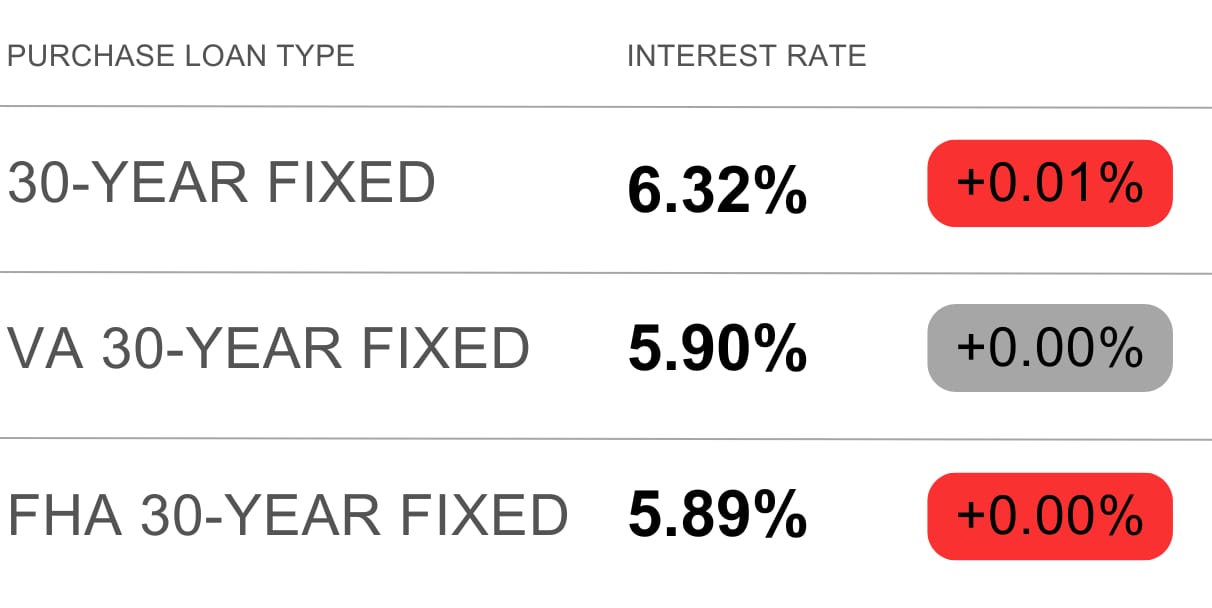

Mortgage rates are pressuring demand: Rates climbed back to ~6.3%–6.4% after briefly dipping below 6%, eroding affordability and keeping buyers on the sidelines.

Prices remain elevated despite weaker sales: The median home price rose 1.4% year over year to $408,800, extending the affordability squeeze even as transaction volume declines.

Inventory is improving, but still constrained: Listings are rising, giving buyers more options, but remain below pre-2020 levels—limiting a full market reset.

Homes are taking longer to sell: Average days on market increased to ~41, reflecting softer demand and more selective buyers.

Regional imbalances persist: The South and Southwest are loosening with higher inventory, while the Northeast and Midwest remain supply-constrained.

Outlook has weakened: The National Association of Realtors cut its 2026 sales forecast from +14% to +4%, pointing to continued near-term softness.

My take

This is shaping up to be a low-velocity spring season rather than a traditionally weak one: inventory is improving, homes are sitting longer, and buyers have more leverage, but demand isn’t responding. Affordability constraints and economic uncertainty are keeping buyers on the sidelines, even as conditions tilt in their favor. As a result, prices remain relatively sticky while transaction volume slows, creating a disconnect between market conditions and actual activity. Until mortgage rates decline meaningfully or buyer confidence returns, the market will likely remain characterized by more options and more negotiating power, but fewer deals getting done.

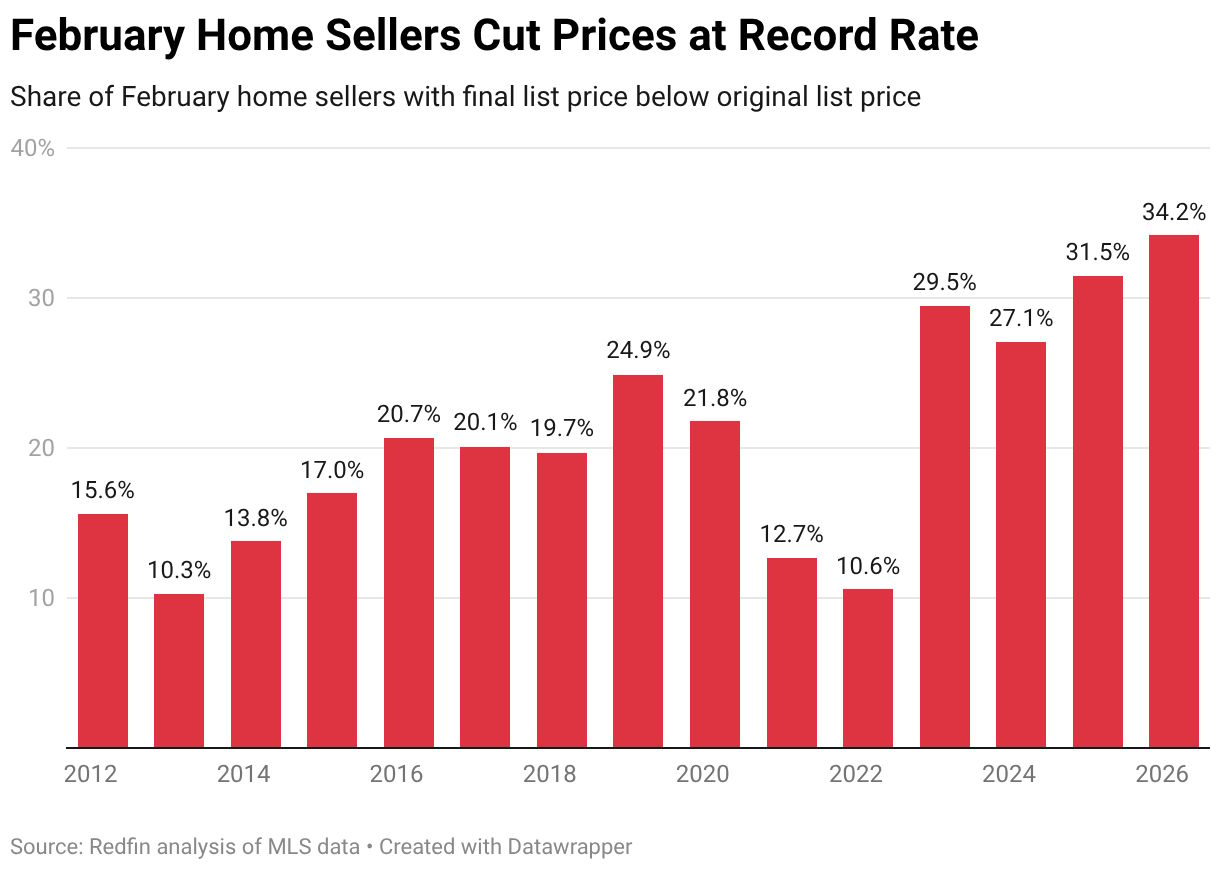

Source: Redfin

More than one-third (34.2%) of February home sellers lowered their list price. That’s up from 31.5% a year earlier and represents the highest February share in records dating back to 2012. That’s according to Redfin's latest update. Here are the key takeaways.

Discounting is becoming more aggressive: Sellers who cut prices reduced them by an average of $40,915 (7.3%), the largest February percentage cut since 2023.

Sun Belt markets are driving the trend: San Antonio (57.9%), Austin (55.2%), and Dallas (47.3%) lead the nation in price cuts, reflecting elevated supply and stronger buyer leverage.

Coastal markets remain more resilient: San Francisco (7.4%) and San Jose (11.1%) have the lowest share of price cuts

April and May are the best times to sell without a price cut: In six of the past 10 years, May was the month with the lowest share of price cuts. April had the lowest share in three of the past 10 years, including 2024 and 2025.

My take

This is what a buyer’s market looks like in practice. Inventory is building, demand is constrained, and sellers are having to compete for attention rather than dictate terms. While spring is typically the window when sellers can avoid cutting prices, we’re glad that more sellers have finally come to terms with reality. In today’s market, pricing correctly from day one isn’t optional—it’s the difference between selling and ending up with a stale listing. Unfortunately, until buyer confidence returns, even well-priced homes may struggle to move. Agents will need to prepare their clients, resetting expectations around pricing, timing, and negotiation.

The most expensive home sales in March

Source: Unsplash

Florida is becoming the epicenter of the ultra-luxury market. Seven of the ten most expensive home sales of March took place there. Ultra-wealthy buyers continue to gravitate toward the state’s tax advantages, waterfront lifestyle, and deep pool of trophy assets.

At the top, a $170 million deal on Indian Creek Island didn’t just lead the list—it reset the bar for Miami-Dade by a wide margin.

Outside of Florida, only a few standout properties in California and Tennessee made the cut, reinforcing how selective buyers are at this level.

Here are the most expensive U.S. home sales of March, according to Redfin:

7 Indian Creek Island Rd., Indian Creek, FL 33154: Sold for $170 million

1460 Ocean Blvd., Manalapan, FL 33462: Sold for $51.2 million

1111 Calle Vista Dr., Beverly Hills, 90210: Sold for $47 million

9111 Collins Ave. Unit N-PH6, Surfside, FL 33154: Sold for $44 million

870 S. Ocean Blvd., Palm Beach, FL 33480: Sold for $37.1 million

160 Clarendon Ave., Palm Beach, FL 33480: Sold for $36 million

998 Dickinson Ln., Franklin, TN 37069: Sold for $35 million

6480 Allison Rd., Miami Beach, FL 33141: Sold for $33.3 million

190 Almendral Ave., Atherton, CA 94027: Sold for $32.5 million

387 Ocean Blvd., Golden Beach, FL 33160: Sold for $32.5 million

My take

The trend we saw in 2025 is repeating in 2026. The broader market is having a tough time, but the ultraluxury market isn’t. It’s still hot. $100 million-plus deals are no longer one-off events. Since the pandemic, there have been an average of 40 home sales a year above $50 million. Wealthy buyers – insulated from mortgage rates, inventory constraints, and affordability pressures – are using real estate to park money, diversify their portfolios, and hedge against inflation. As long as our K-shaped economy sticks around, it’s hard to see this trend changing anytime soon. Right now, the ultraluxury market has all the momentum.

Schematics

The news that just missed the cut

Source: Unsplash

SERHANT has now launched operations in California

Use this script to get hesitant sellers off the fence to list with you

The best AI tools for real estate agents, according to HousingWire

Homebuilders are now resorting to this to maintain profits in a stagnant market

Real talk: agents open up about why and when they had to fire their clients

Foundation Plans

Advice from David to win the day

As we mentioned up top, we’re living through a mismatched market right now.

On paper, this is a buyer’s market: inventory is up, and sellers are willing to cut prices and offer other concessions. But in practice, buyers aren’t stepping in. They’re not just thinking about price anymore; they’re thinking about uncertainty: rates, inflation, job security. That uncertainty is keeping them on the sidelines. Nearly 30% of Americans say they’re delaying major purchases, including homes.

Over the next few weeks, we’ll break down how to navigate this environment. Today, we’ll start with two practical shifts you can make right now:

1. Help buyers get some perspective – Start by acknowledging what your clients are feeling. Don’t try to dismiss it; they’re reacting to real headlines. But your job isn’t just to validate concern; it’s to bring clarity.

Use your emotional intelligence to help clients understand where they actually stand, not just how they feel. Give them context. For example, on mortgage rates:

Average 30-Year Mortgage Rate in the US

1970s: 8.9%

1980s: 12.7%

1990s: 8.1%

2000s: 6.3%

2010s: 4.1%

2020s: 5.3%

All-Time Low (Jan 2021): 2.65%

2023 Peak (Oct 2023): 7.79%

Today's Rate: 6.32%

The goal isn’t to argue that today’s rates are “low”— it’s to show they’re not unprecedented. When people get nervous, they either freeze or rush. Right now, most are freezing. Your role is to slow things down, reframe the moment, and replace emotion with clarity.

The more clarity you provide, the more confident they’ll feel moving forward.

2. Start acting like a dealmaker – Even in moments of crisis and uncertainty, deals still get done. They don’t stop; they concentrate.

What happens is that the casual buyer and investor fall by the wayside, leaving a smaller group of serious operators who move fast, decide quickly, and keep transacting regardless of conditions. The agents who win aren't chasing the broader market; they're identifying these players, building relationships with them, and helping them execute repeatedly.

If you want stability, stop waiting for better conditions for the market to “come back.” Instead, align yourself with the people who transact. Study who’s doing deals in your market. Get in front of them and position yourself as someone who makes their business easier.

Stop acting like an order taker. Start acting like a dealmaker.

Just in Case

Keep the latest industry data in your back pocket with today’s mortgage rates:

Source: Mortgage News Daily

“Just because you are doing a lot more doesn't mean you are getting a lot done. Don't confuse movement with progress!” — Denzel Washington

Progress isn’t about doing more, it’s about doing what matters most. Be intentional and focused in what you choose to do, friends. That’s how you build the business and life you want.

Have a wonderful week. We’ll see you back here on Friday!

- David